The landscape of commerce has shifted dramatically, moving from tactile transactions to an increasingly invisible flow of digital value. This isn't just a minor tweak; it's a fundamental reimagining of how money moves, driven by The Evolution of Virtual Card Technology & Digital Payments. For businesses and individuals alike, understanding this acceleration isn't merely an advantage—it's essential for security, efficiency, and growth in a globalized, always-on economy.

What once felt like a futuristic concept is now the backbone of modern financial operations. From protecting online purchases with single-use credentials to streamlining complex B2B payments, virtual cards and the broader digital payment ecosystem are reshaping our financial reality, making transactions faster, safer, and remarkably more controllable.

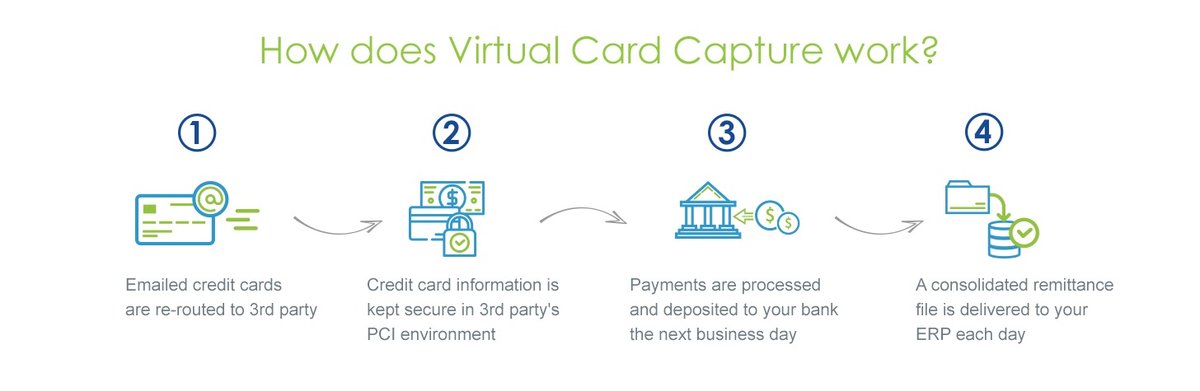

At a Glance: Why Virtual Cards & Digital Payments Matter Now More Than Ever

- Enhanced Security: Protect against fraud with unique, temporary card numbers.

- Unrivaled Control: Set precise spending limits, dates, and merchant restrictions.

- Streamlined Operations: Automate reconciliation and expense tracking.

- Increased Efficiency: Accelerate payment processing for faster cash flow.

- Global Reach: Facilitate secure cross-border transactions with ease.

- Future-Proofing: Embrace technologies like AI and embedded finance for competitive advantage.

From Physical Wallets to Digital Flows: The Genesis of Modern Payments

Remember a time when a thick leather wallet, stuffed with plastic cards, was your primary financial conduit? That era, while not entirely gone, is rapidly receding into the rearview mirror. The journey began with the shift from cash to credit and debit cards, bringing convenience but also introducing new vulnerabilities. Early digital payments, often tied directly to these physical cards, offered a taste of frictionless commerce online but still carried the inherent risks of sharing primary account numbers.

The real revolution kicked off when innovators started to decouple the card number from the physical plastic. Mobile payments, online banking portals, and digital wallets laid the groundwork, training users to trust their screens with their money. This trust, combined with an urgent need for greater security in an increasingly online world, naturally paved the way for the concept of virtual cards. They emerged not just as an alternative but as an essential layer of protection and control, perfectly suited for the demands of the digital age.

Virtual Cards: Redefining Security and Control in the Digital Realm

So, what exactly is a virtual card? At its core, a virtual card is a unique, randomly generated 16-digit payment card number, complete with its own expiration date and CVV, that isn't tied to a physical piece of plastic. It's essentially a digital token that represents your actual payment account, but with a crucial difference: it provides an extra layer of abstraction and control. Think of it as a disposable (or highly controlled) digital alias for your primary card.

How Virtual Cards Work Their Magic

When you request a virtual card, your bank or payment provider generates a unique card number. This number can be configured with specific parameters, making it incredibly versatile:

- Single-Use or Multi-Use: A virtual card can be designed for a single transaction, expiring immediately after use, or for multiple transactions over a set period (e.g., for a recurring subscription).

- Spending Limits: You can impose strict limits on how much can be spent using that specific virtual card, preventing overspending or unauthorized large purchases.

- Merchant Restrictions: Some systems allow you to tie a virtual card to a specific merchant or merchant category, ensuring it can only be used where intended.

- Date & Time Restrictions: You can set expiration dates, or even specific time windows, for when a virtual card is valid.

- Tokenization: The underlying technology often uses tokenization, replacing sensitive card details with a unique identifier (token) during transactions. If a token is compromised, the actual card details remain secure.

This granular control is a game-changer. Imagine issuing a virtual card to an employee for a specific software subscription, limiting it to that vendor and amount, or using a unique virtual card for every online purchase to insulate your primary card number from potential data breaches. The peace of mind is invaluable.

Beyond Security: The Business Transformation Powered by Virtual Payments

While security is a primary driver, the true power of virtual cards lies in their ability to transform business operations, especially in complex B2B environments. They move beyond simple transaction protection to become strategic tools for financial management.

Key Business Use Cases and Benefits:

- Automated Expense Management: Businesses can issue virtual cards to employees for specific expenses (travel, software, supplies). Each card can have predefined limits and categories, ensuring compliance and simplifying reconciliation. Expense reports practically write themselves.

- Streamlined Vendor Payments: Paying multiple vendors? Issue a unique virtual card for each supplier, or even for each invoice. This makes tracking spending per vendor effortless and provides a clear audit trail.

- Subscription Management: Control recurring software subscriptions or SaaS tools by issuing dedicated virtual cards for each. If a service needs to be canceled, you can simply deactivate the card without updating details across multiple vendors.

- Fraud Prevention & Risk Mitigation: By isolating transactions with unique virtual numbers, the impact of a data breach is minimized. If one virtual card is compromised, only that specific card needs to be canceled, not your primary corporate account.

- Enhanced Reporting and Analytics: Because each virtual card can be tagged with specific project codes, departments, or purposes, financial teams gain unprecedented visibility into spending. This data feeds into more accurate budgeting, forecasting, and audit processes.

- Operational Efficiency: The ability to instantly generate and distribute payment methods reduces administrative overhead, eliminates manual payment processes, and accelerates the entire payment cycle. This speed translates directly into better cash flow management and stronger vendor relationships.

Need to generate virtual cards quickly for your team or specific projects? Many platforms now offer robust tools for this. When seeking ways to streamline your payment processes and enhance security, knowing where to find such resources is key. Access the VCC generator to empower your business with immediate, secure payment solutions.

The Digital Payments Ecosystem: A Broader Interplay

Virtual cards don't exist in a vacuum. They are a critical component of a much larger and rapidly evolving digital payments ecosystem. This ecosystem includes:

- Mobile Wallets (Apple Pay, Google Pay): While often housing tokenized versions of physical cards, they can also store and use virtual card numbers for in-store or in-app purchases, bridging the gap between online and offline.

- Real-Time Payments (RTP): Systems like FedNow in the US or SEPA Instant in Europe enable instant fund transfers between bank accounts. While different from card payments, they contribute to the expectation of speed in all financial transactions, pushing card networks to innovate.

- APIs (Application Programming Interfaces): These are the connective tissue of modern finance. APIs allow different systems to talk to each other, enabling seamless integration of virtual card generation into existing accounting software, ERPs, or expense management platforms. This programmatic access is where much of the efficiency gains are realized.

- Payment Orchestration Platforms: For businesses dealing with multiple payment methods, currencies, and geographies, orchestration platforms provide a single hub to manage everything. Virtual cards fit perfectly into this framework, offering flexible payment routing and provider diversification.

This interconnectedness means that advancements in one area often accelerate progress in others. The demand for instant, secure, and data-rich transactions drives innovation across the board.

The AI Accelerant: Pushing the Boundaries of Digital Payments

Artificial intelligence (AI) is no longer confined to science fiction; it's rapidly becoming an integral part of our daily lives, and its impact on virtual card technology and digital payments is profound. The PYMNTS report on AI's future highlights how predictive analytics in finance are rapidly enhancing efficiency and convenience. This trend directly fuels the next generation of digital payments and virtual card capabilities, making them smarter, safer, and more personalized.

How AI Is Revolutionizing Virtual Cards and Payments:

- Next-Gen Fraud Detection: AI algorithms can analyze vast datasets in real-time to identify anomalous spending patterns with incredible accuracy. This moves beyond rule-based systems to proactively detect and prevent sophisticated fraud attempts on virtual cards, often before they even register as suspicious to a human.

- Dynamic Spending Limits: Imagine a virtual card that automatically adjusts its spending limit based on real-time factors like an employee's historical spending, project budget, or even market conditions. AI can enable this dynamic control, optimizing spend without constant manual intervention.

- Personalized Payment Experiences: AI can analyze user preferences and behaviors to suggest the most convenient and cost-effective payment methods, or even to pre-populate virtual card details for frequently used vendors, streamlining the checkout process.

- Automated Reconciliation and Categorization: AI-powered tools can automatically match transactions to invoices, categorize expenses, and even identify discrepancies, drastically reducing the manual effort required for financial reconciliation. This transforms accounting from a reactive process into a proactive one.

- Optimizing B2B Workflows: From intelligent invoice processing to predicting cash flow needs, AI can optimize every step of the B2B payment journey, making virtual cards an even more powerful tool for treasury and procurement teams.

- Enhanced Customer Service: AI-powered chatbots and virtual assistants can help users generate virtual cards, troubleshoot issues, or provide real-time spending insights, improving the overall user experience.

The ethical implications of widespread AI adoption, such as data privacy and algorithmic bias, cannot be ignored, as the PYMNTS report also notes. Responsible development and deployment of AI in financial services are crucial to ensure these advancements benefit everyone fairly and securely.

Challenges and Considerations: Navigating the Digital Payment Landscape

While the benefits of virtual card technology and digital payments are clear, the path to full adoption isn't without its hurdles.

- Legacy System Integration: Many businesses, especially larger enterprises, operate with older financial systems that aren't designed for seamless API integration or real-time data flows. Migrating or integrating these systems can be complex, costly, and time-consuming.

- Security Concerns and Data Privacy: Despite their inherent security advantages, any digital payment system introduces new vectors for attack. Continuous vigilance, robust encryption, and adherence to data privacy regulations (like GDPR or CCPA) are paramount. The ethical concerns around data privacy highlighted in the AI report are particularly relevant here.

- User Adoption and Training: Shifting employees and customers away from familiar physical cards or traditional payment methods requires education and clear communication. Training programs are essential to ensure users understand how to effectively and securely use virtual cards.

- Regulatory Compliance: The payments industry is heavily regulated. As digital payments evolve, compliance with anti-money laundering (AML), know-your-customer (KYC), and other financial regulations becomes even more complex, especially across international borders.

- Scalability: As businesses grow, their digital payment infrastructure must scale with them. Choosing solutions that can handle increasing transaction volumes and expand functionality is crucial for long-term success.

Addressing these challenges requires a strategic approach, a willingness to invest in technology, and a commitment to ongoing education and adaptation.

The Future is Now: Emerging Trends in Digital Payments

The evolution of virtual card technology and digital payments is far from over. Several key trends are shaping what comes next, promising even greater integration and innovation:

- Embedded Finance: Payments are disappearing into the background, becoming an invisible part of the user experience. Imagine ordering office supplies, and the payment is automatically handled by a virtual card tied to that specific vendor and budget, without you ever explicitly "paying."

- Programmable Money: The ability to attach conditions and logic directly to money itself. Virtual cards already offer a glimpse of this with their spending limits and merchant restrictions, but future iterations could see even more sophisticated "smart contracts" dictating how and when funds can be used.

- Blockchain and Distributed Ledger Technology (DLT): While still nascent in mainstream payments, DLT has the potential to offer immutable, transparent, and highly secure transaction records, which could enhance the backbone of future digital payment systems.

- Hyper-Personalization: Leveraging AI, payments will become increasingly tailored to individual preferences and behaviors, offering bespoke solutions for budgeting, rewards, and even credit offerings.

- Cross-Border Simplification: Expect continued innovation in making international payments as seamless and cost-effective as domestic ones, with virtual cards playing a key role in managing foreign exchange risk and compliance.

Making the Shift: Practical Advice for Businesses

Embracing the evolution of virtual card technology and digital payments is not just about keeping up; it's about gaining a competitive edge. Here's how to approach it:

- Assess Your Current State: Start by analyzing your existing payment processes. Where are the bottlenecks? What are your biggest fraud risks? How much time do you spend on reconciliation? This will highlight where virtual cards can deliver the most immediate impact.

- Define Your Needs: Identify specific use cases. Do you need better expense management for employees? More control over vendor payments? Improved security for online advertising spend? Clearly defined goals will guide your solution selection.

- Research and Choose a Provider: The market offers a wide range of virtual card providers, from dedicated platforms to services integrated into larger banking or ERP systems. Look for features like API capabilities, integration with your existing software, robust reporting, strong security protocols, and responsive customer support.

- Start Small, Scale Smart: Consider piloting virtual cards with a specific team, department, or for a particular type of expense. This allows you to test the system, gather feedback, and refine your processes before a wider rollout.

- Invest in Training and Communication: A successful transition relies on user adoption. Develop clear training materials, offer workshops, and communicate the benefits to your team. Show them how virtual cards will make their jobs easier and more secure.

- Monitor and Optimize: Digital payments are dynamic. Continuously monitor your virtual card usage, analyze the data, and look for opportunities to optimize limits, categories, and workflows. Stay informed about new features and security best practices.

Common Questions About Virtual Cards & Digital Payments

Are virtual cards truly safer than physical cards?

Yes, generally. Virtual cards offer several layers of security that physical cards don't. Their unique numbers limit exposure, single-use options prevent reuse if compromised, and you can impose strict spending limits. If a virtual card is breached, your primary account number remains secure.

Can I use a virtual card for anything?

Most online transactions that accept credit/debit cards can accept virtual cards. Some physical point-of-sale systems might accept them if integrated with mobile wallets (e.g., Apple Pay or Google Pay) that store your virtual card. However, they're not ideal for situations requiring a physical card for verification (like hotel check-ins or car rentals, though this is changing).

What’s the difference between a virtual card and a mobile wallet?

A mobile wallet (like Apple Pay or Google Pay) is a container that stores various payment methods, including tokenized versions of your physical cards or even virtual cards. A virtual card is a specific type of payment credential that lacks a physical form. You can have virtual cards within a mobile wallet.

How do virtual cards help with budgeting?

Virtual cards are excellent for budgeting because they allow you to set specific spending limits for different categories or projects. For example, you could issue a virtual card with a $500 limit for office supplies each month, ensuring you never exceed that budget. The granular transaction data also simplifies tracking and reconciliation.

Your Next Step in the Digital Payment Journey

The rapid pace of innovation in digital payments, particularly with virtual card technology, isn't slowing down. Ignoring these advancements risks leaving your business vulnerable, inefficient, and behind the curve. Instead, embrace this evolution as an opportunity.

Start by exploring the tools available, assess how virtual cards can solve your specific security, control, and efficiency challenges, and then take that first step towards a more secure and streamlined financial future. The journey to fully digital, AI-powered payments is ongoing, but the immediate benefits of integrating virtual card technology are already here for the taking. The future of payments isn't coming; it's already accelerating, and you have the power to drive along with it.